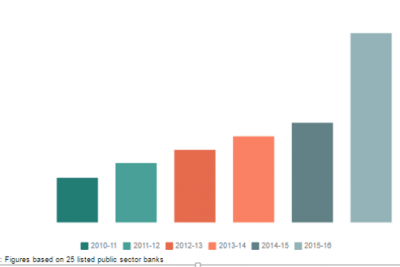

(Source: Capital-line)

The above figure shows the rising trend of NPA’s in the banking system, especially in the public sector banks. The rising NPA are the cause of dampening the investor’s sentiments. Due to the rise in NPA, the banks will have to keep aside more money as a provision which in turn will affect its liquidity and profitability. The galloping increase in NPA’s in the Indian banking system has been the reason of higher interest rates on new loans as the banks have to maintain their profitability and manage their capital losses.

The major victims of this rising NPA’s were the public sector banks. The net profit of SBI fell by 62% in the December 2015 quarter and that of Union Bank of India declined by 74%. However, some small players like Yes Bank, due to its size of operations remained immune to this epidemic. Yes Bank reported a 27 percent increase in its profit in March 2016 quarter as the non-performing assets were a meager 0.8% of its total loan.

The sectors contributing to the growth of NPA’s are mining, aviation, infrastructure and textile. Not only Priority Sector Lending (PSL) but the corporate sector also led to the increase in bad loans. Relaxation of lending norms, sluggish legal and governing system made it difficult for the banks to recover their funds from corporate as well as non-corporate sector.

The growth of NPA’s has outpaced the economic growth of India. They not only hinder the prospects of lower interest rates but also pull down the implementation of several government schemes that hinge on banking services. The increasing NPA’s in the banks are getting global and being deciphered as a major flaw in the existing Indian Government. The PSB bad loans grew from Rs.3.09 lakh crore to Rs.5.8 lakh crore in the last one year only. Due to rising NPA’s, the capital base of major banks are shrinking and this results in higher interest rates and investors are also losing interest in banks.

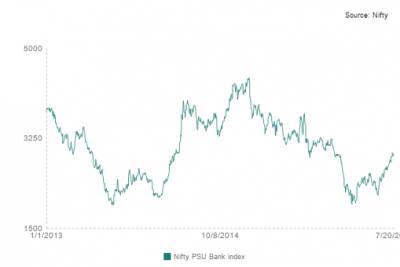

The banking stocks were also not saved from the alarming effect of rising NPA’s. The effects on the stocks are shown by the following graph-

(Source-Nifty)

To revamp the existing banking system, Reserve Bank of India in confluence with the Central Government has decided to adopt measures to clean up the bank's books. Instead of expecting to recover the loans in future, which remain a far-fetched dream they are finding a viable long-term solution. In the absence of this, the bank sector will undergo a real crisis and the dangers of losing the market will prevail. RBI has introduced a comprehensive “Framework for Revitalizing Distressed Assets in the Economy” and strategic debt restructuring which will allow lending banks to convert loans into equity if a borrower fails to adhere to the set norms. The RBI has also revamped the 5/25 scheme. RBI has set the deadline for banks to reach a healthy capital adequacy by 2019 and has stressed on strict conformance with BASEL III norms.

The Central Government has also adopted measures against these loan defaulters to instill in them the importance of public money by using various Acts like the Prevention of Corruption Act, amendments in the SARFAESI Act, introducing a recapitalization package, amending the bankruptcy code which will act as a catalyst to legal solutions and thus supplement RBI’s efforts. The seven-point directive “Indradhanush” has been a confidence building measure among the Government of India, the Reserve Bank of India and the Public Sector Banks.

Comments