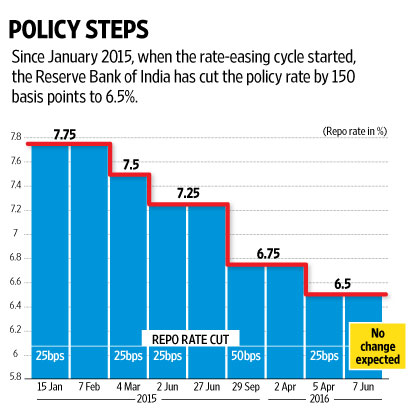

This time around, Rajan is expected to refrain from cutting the policy rate and opt for the status quo. Since January 2015, when the rate-easing cycle started, RBI has cut the policy rate by 150 basis points to 6.5%.

One basis point is one-hundredth of a percentage point.

Between April 2016, when the Indian central bank cut its policy rate by 25 basis points, and now, nothing significant has happened that warrants any change either in the policy rate or its stance in the June policy.

Retail inflation surprised everybody by quickening in April to 5.4% from 4.8% in the previous month, driven primarily by food inflation even as so-called core inflation, or non-food, non-oil, manufacturing inflation, remained relatively steady. This is also much higher than the average inflation of 4.9% in fiscal year 2016 that ended in March.

Wholesale inflation, which has little relevance in RBI’s scheme of things, was 0.3% in April, after being in negative territory for 18 months. Higher food inflation and a surge in commodity prices contributed to it.

Indeed, India’s factory output in March was much weaker than anticipated—just 0.1% after expanding by 2% in February.

But the disappointment was more than offset by the 7.9% growth that the Indian economy clocked in the March quarter, surprising all. Annual growth, however, remained unchanged at 7.6%, because of a downward revision for the first three quarters. The $2 trillion economy has chugged along, riding on an improved agricultural performance and robust growth in mining, quarrying, electricity and construction. Many are cynical about the growth figures, but there is no denying the fact the worst is probably behind us.

All eyes now will be on the progress of the monsoon which is expected to be normal or slightly above normal after two years of drought. On the external sector, the key factor on which RBI is keeping a close watch is surging oil prices. Since the last policy, crude prices have risen by around 30% and, in the past five months, since January, the rise is at least 60%, triggered by supply disruptions in Libya and Nigeria—holders of Africa’s largest crude reserve. Rising prices of crude impact inflation, and a further rise from the current level is not entirely ruled out.

However, what may give RBI comfort on its “accommodative” monetary stance is the latest US job data. In the past few weeks, expectations of a US Fed Reserve rate hike in June or July have risen (from less than 10% chance to more than 50%), putting pressure on emerging-market currencies and strengthening the greenback. The scenario dramatically changed on 3 June after it was found that the US economy created in May the fewest jobs in more than five-and-a-half years, as manufacturing and construction employment fell sharply. Non-farm payrolls increased by only 38,000 jobs last month—the smallest gain since September 2010. The Fed had indicated that it would raise rates soon if there was no slowdown in job creation and if other economic parameters convince the US central bank that indeed there is a pickup in growth in the second quarter.

In fact, on 27 May, at Harvard University in Cambridge, Massachusetts, Fed chair Janet Yellen said the ongoing improvement in the US economy would warrant another interest rate increase “in the coming months”, almost dropping a hint that the Fed would act in June when its policymaking body, the Federal Open Market Committee (FOMC), meets. The Fed hiked its policy rate in December for the first time in nearly a decade.

Clearly, while presenting the June policy, RBI does not have any dilemma. It can wait and watch how the monsoon pans out, the price of crude and the US Fed action, besides inflation data, before taking a decision on whether or not to make what would probably be the last rate cut in the months to come. Meanwhile, it is keeping a hawk eye on the impact of the change in its stance on liquidity and Indian banks shifting from the base rate, or minimum loan rate based on average cost of money, to a dynamic marginal cost-based lending where the loan rate can change every month.

Since it was introduced in April, banks have been slowly paring their rates by a few basis points every month even as liquidity deficit is easing. The RBI has released Rs.70,000 crore into the system by buying bonds from the market through the so-called open market operations in the past two months (comparable figure for the entire fiscal year 2015-16 was Rs.54,000 crore). The daily liquidity deficit, which was about Rs.2.5 trillion for some days in March, has come down dramatically.

This will ease further once RBI pays dividend to the government in August.

With the ease in liquidity, the banks will continue to cut their loan rates, but the pace will gain momentum only after they fully absorb the impact of close to $26 billion redemption of foreign currency non-resident (FCNR) deposits, beginning September. Indian banks raised this money overseas to support the rupee, which came under pressure in September 2013 and swapped it with the central bank.

This means the banks raised dollar deposits and sold them to RBI for rupees; now they would return the money to the central bank and get back the dollars to redeem the deposits at maturity.

Even though Rajan has said that RBI is fully prepared for the redemption and it has hedged its position in the forwards market, analysts do not seem entirely convinced. The redemption may have an impact on banks’ rupee liquidity; they will be more aggressive in rate cuts only after clarity emerges on this front.

The gap between RBI’s policy rate and the banks’ average one-year loan rate is now around 270-275 basis points. This gap is expected to come down to about 225 bps if the dollar deposit redemption does not face any hiccup, and, even after the outflow, banks do not suffer from any liquidity crunch. One can expect a drop of about 50 basis points in loan rates by the end of 2016 even if RBI does not cut its policy rate any further.

There is one caveat though: Rajan calling it a day at RBI will disrupt this calculation. How long the disruption will last depends on the state of the economy when the market gets to know the little secret which the Indian government is keeping close to its chest.

---------

* This column originally appeared in Mint

About the Author:

Tamal Bandyopadhyay is one of the most respected business journalists in India. Currently, he is a Consulting Editor of Mint, writes a weekly column on Mint - Banker's Trust, which is widely read for its deep insights into the world of finance. He is also an Adviser on Strategy for Bandhan Bank. He has authored two best sellers on finance, `A Bank for the Buck' and `Sahara: The Untold Story'. His latest book, `Bandhan: The Making of a Bank," a Penguin publication, is being released in June.

Comments