It’s February and I hope everyone would have commenced planning about the closure of their books of accounts. The most important aspect that needs consideration while planning is how to effectively reduce one’s income-tax liability for the current year (FY 2013).

( Promoted : All articles by CA Prince Doshi, Tax Planning services by Prince Doshi)

From an income-tax perspective, there is a slight distinction between the terms ‘exemption’ and ‘deduction’ which are often used interchangeably by the tax payers. Exemption refers to the component of the taxpayer's income which is exempt from tax ie taxes are not to be paid in respect of that particular income. Deduction refers to the amount resulting in reduction of the total income of the taxpayer thereby reducing the tax liability. Income-tax planning vests on the deduction claimed from the gross total income of the taxpayer.

Illustrated below are some of the common modes of deductions that can and should be availed of by every taxpayer to reduce his/her tax liability:

A. Under Section 80C read with Section 80 CCE of Income Tax Act, 1961 (‘Act’)

- Life Insurance Premium

- Available to an individual in respect of the premiums paid for self, spouse or their children –premiums paid for parents is not allowed as deduction

- Available to an HUF in respect of the premiums paid for any member of the HUF

- Insurance premium should not exceed 20% of the actual capital sum assured (generally ignored by taxpayers while claiming deductions) and should be continued to be paid for at least 2 years

2. Fixed Deposit (‘FD’)

- FD should be with a scheduled bank (instance - State Bank of India) for a period of 5 years

- The rate of interest is generally 8.5%, but the tax benefit available with regards to the deposit amount effectively increases the rate of return

3. Contributions to Public Provident Fund (‘PPF’)

- Available to an individual for self, spouse and children and to HUF for any member of HUF

- The rate of interest provided by PPF is low but the interest income earned is exempt from tax thereby effectively enhancing the rate of return

- Maximum amount that can be deposited in a PPF a/c during a FY is Rs 100,000 (earlier it was Rs 70,000)

4. Mutual Funds (‘MF’) – commonly referred as ELSS

- Subscriptions to the units of MF referred under Section 10(23D) of the Act are allowed

- The units should not be sold within the lock-in period as per the MF scheme

5. Tuition fees

- Educational fees paid to any university, college or school within India for the purpose of full time education – fees paid to coaching classes or other private tuitions are not permissible deductions

- Deduction will be allowed in respect of fees paid for only two children

6. Cost of purchase or construction of a residential house property

- The principal repayment of loan taken from an approved financial institution for the purpose of purchasing a residential house property

- The residential property should be not sold within 5 years from the end of the financial year in which the property is purchased

There are several other means which qualify for deduction but are not usually opted for – for instance premiums paid to keep a deferred annuity contract in force, subscription to NABARD bonds, post office deposits, contributions to NSC (VIII issue) etc

The maximum amount of deduction that can be availed using all the aforesaid modes is Rs 100,000.

B. Under Section 80D / 80DD / 80DDB Act

- Mediclaim premium

- Available to an individual in respect of the mediclaim premiums paid for self, spouse, dependent children or dependent parents – premium paid for parents is also allowed as deduction (varies from the LIC premium criteria as discussed above) and to HUF in respect of premiums paid for any member of the HUF

- Premium should be paid in any mode except cash, from taxable income of the taxpayer

- Deduction limit – Rs 15,000 (Rs 20,000 in case the taxpayer is senior citizen ie aged above 60) in case of premium paid for self, spouse or dependent children plus Rs 15,000 in respect of premiums paid for parents (Rs 20,000 in case parents are senior citizens). Effectively, a maximum deduction of Rs 40,000 can be availed by a senior citizen taxpayer and Rs 35,000 by a non-senior citizen.

2. Medical expenditure for disable or handicapped dependent

- Available to an individual or an HUF in respect of either medical expenditure incurred on medical treatment of or for the deposits for future needs of the disabled or handicapped dependent - self, spouse, parents, children, brothers and sisters

- Maximum deduction – Rs 40,000 (Rs 100,000 in case of disability of more than 80%)

- Obtaining a medical certificate of the same is essential

3. Medical treatment for serious ailments

- Available to an individual or an HUF in respect of expenditure incurred for the medical treatment of a specified disease / ailment (instance Cancer, Aids, etc) for self or any dependent - spouse, parents, children, brothers and sisters

- Amount of deduction is Rs 40,000 (Rs 60,000 in case the patient is senior citizen) or amount actually spent whichever is less

- Obtaining a medical certificate of the same is essential

C. Under Section 80E of the Act

- Interest on education loan – refer my previous article http://insideiim.com/all-you-need-to-know-about-tax-benefits-on-education-loan-interest-payments/

D.

Under Section 80G / 80GG of the Act

- Donations

- Available to all taxpayers (individuals, HUF, corporate, firms) in respect of donation made to certain specified institution and associations

- The amount of deduction shall be either 100% or 50% of the donation amount depending on the sanctioned status of the institution or association to whom donation is made

2. Rent paid

- Available to all taxpayers paying rent and are not in receipt of any House Rent Allowance (‘HRA’)

- Allowable only to those taxpayers who do not own any residential accommodation and are paying rent for the accommodation which is occupied for their own residence

- The amount of deduction is Rs 2,000 p.m. or 25% of the total income of the taxpayer, whichever is less

E. Under Section 80 TTA of the Act

- Interest from savings bank account (inserted recently effective from April 1, 2012 pertaining to FY 2012‑13)

- Available to an individual or HUF in respect of interest income earned from deposits in the bank savings account opened with a bank covered under the Banking Regulations Act

- Amount of deduction will be the bank interest amount or Rs 10,000 whichever is less

F. Under Section 80CCG of the Act

- Investment in equity shares – Rajiv Gandhi Equity Savings Scheme (inserted recently effective from April 1, 2012 pertaining to FY 2012‑13)

- Available only to a resident individual taxpayer in respect of listed equity shares acquired by him during the financial year 2012-13 – not available to HUF

- Gross total income of the individual taxpayer should not exceed Rs 10,00,000

- The taxpayer should be a new individual retail investor – ie the taxpayer who may have opened a demat account but have not made any transaction in equity and/or in derivatives till the date of notification of this scheme ie November 23, 2012

- Investment should be made only in the specified listed equity shares (BSE 100 / CNX 100) with a fixed lock-in period of 1 year from the date of purchase and flexible lock-in period of another 2 yrs

- Amount of deduction shall be 50% of the amount invested or Rs 25,000 whichever is less

- Currently, deduction is available only for the present FY 2012-13

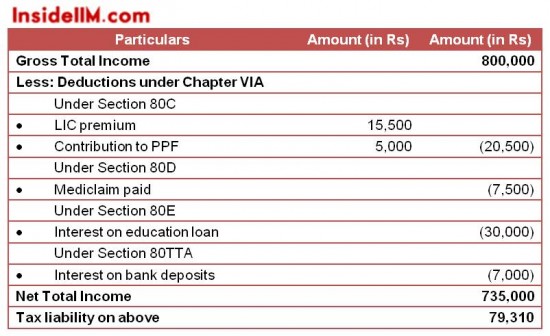

Let’s take an illustrative example where your gross total income is Rs 800,000 (including bank interest of Rs 7,000). During the current FY 2012-13, you have made investments as under:

LIC premium – Rs 15,500 (paid fro self), Mediclaim premium – Rs 7,500 (paid for self), contributions made to PPF – Rs 5,000, interest on education loan paid – Rs 30,000. Your total taxable income and tax liability would be as under:

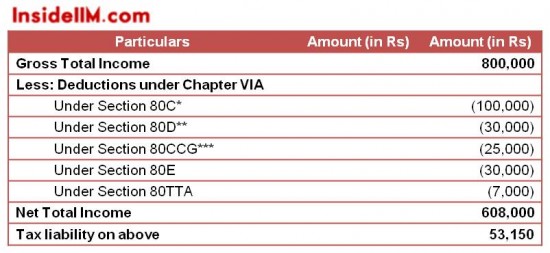

By availing appropriate deductions, the tax liability can be reduced as under:

*Invest more in PPF / Bank FD

**Pay Mediclaim premium for parents from your bank account

***Opt for RGESS scheme, if applicable in your case

{kind=link}

{kind=link}

{kind=link}