The screws are

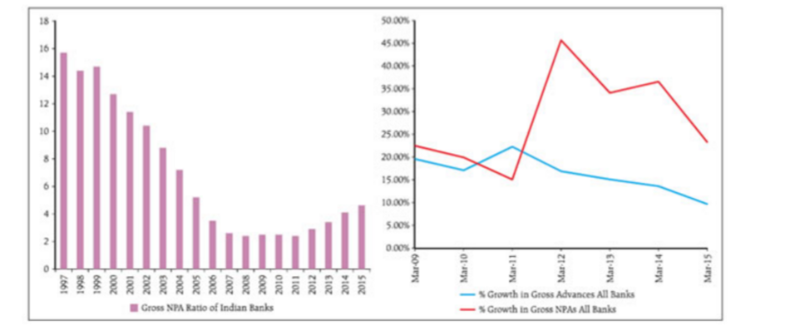

tightening around Mr. Mallya finally with banks asking the Supreme Court to prevent Mr. Mallya from leaving the country. Mr. Mallya is just one example of a long list of other rich and powerful clients who appeared to have indulged in a borrowing binge and now are unable to pay back PSU banks. As a result, non-performing assets of banks has seen an upward trend since 2011 (Source: RBI) and this kept increasing until 2015.

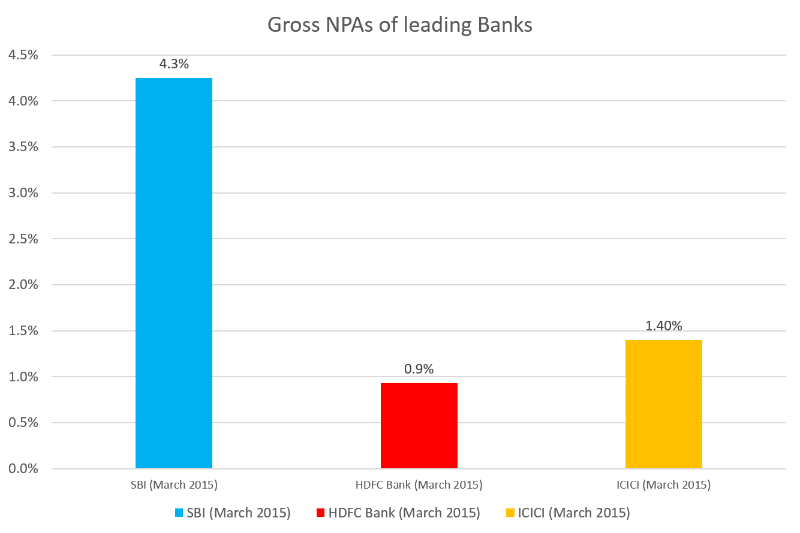

When you look at some of the leading PSU and Private sector banks, it is fairly clear where the problem is emanating from (This has been recognized by numerous analysts and the current Govt as well). Most of the bad loans come from the PSU bank portfolio. In the example below, the state owned SBI is significantly ahead on gross non performing assets (NPA) versus the best managed bank (HDFC Bank). However, it is interesting to note that even the private ICICI bank has a much higher gross NPA than HDFC Bank.

What is it about these banks lending practices that differentiates these banks?

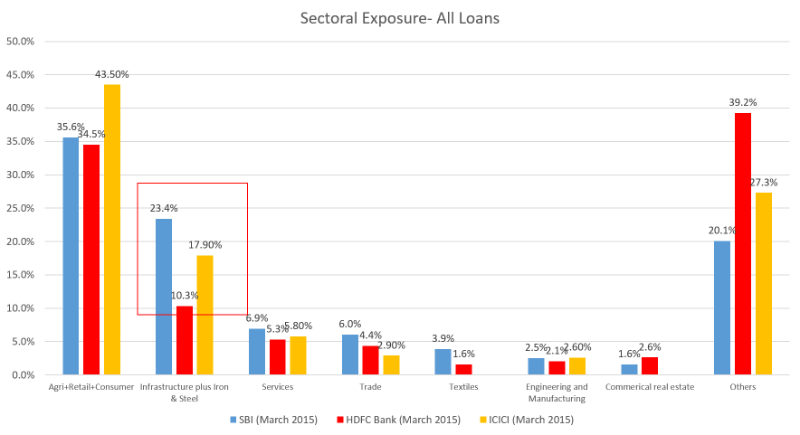

One obvious metric is to look at where these banks are lending?

It is clear from the chart below that the biggest difference comes from Infrastructure (Power, Infrastructure and Telecom) as well as Iron & Steel. SBI lends the most followed by ICICI and HDFC Bank. SBI and ICICI are a lot closer while HDFC is significantly lower. An example probably of prudent lending practices by HDFC Bank.

What is common amongst these sectors?

All of them involve Govt intervention. Roads and Power are closely linked to Govt contracts, Telecom to Govt auctions and regulations and Iron & Steel to auctions, permissions and of course Global commodity prices. Essentially, sectors that involve higher Govt involvement also tend to probably cause more losses to banks (This has been recognised by the ministry in the Indhradhanush document)

Final question, why does SBI have so much more losses than ICICI Bank inspite of having only 6% points more exposure?

That in my view is the most important question that the Government must investigate and answer. In my view, the gap in NPAs between ICICI and State Bank of India even after correcting for slightly higher exposure for SBI in Infra et al should not be more 1%. The gap is currently at 2.9%. In other words, 2% or a minimum of Rs 22000 crores of gross NPA is not just a function of business issues but unhealthy lending practices. Extend this to all PSU banks and you could have a range of about Rs 50-75000 crores of questionable lending. I am in no position to say this is crony lending but this is worth investigating.

It is clear that the NDA Government is unlikely to privatize state owned banks given the roll out of

Indradhanush to fix the State owned banks. Indrandhanush includes 7 main points - Setting up a banking board of bureau to reduce interference and delays in appointments, Capitalisation of Banks to ensure that banks are adequately Capitalized, increased empowerment, improving governance, greater accountability, de-stressing investments that are causing NPAs in Banks. Vinod Rai, ex-CAG, was recently appointed as head of Bank Board Bureau.

The efficacy of this program will be best known if the Gross NPAs of banks keeping coming down and the overall margins of PSU banks keep going up. In the meanwhile a thorough investigation of some of these loans will truly take India's governance to the next level.

---

About the author

Subhash Chandra is a Political Consultant. He is the Founder of SC Polling Consultancy and author of the books -

Battle of Bihar and

The Little Book of BIG Customer Satisfaction Measurement.

{kind=link}

{kind=link}

{kind=link}

{kind=link}