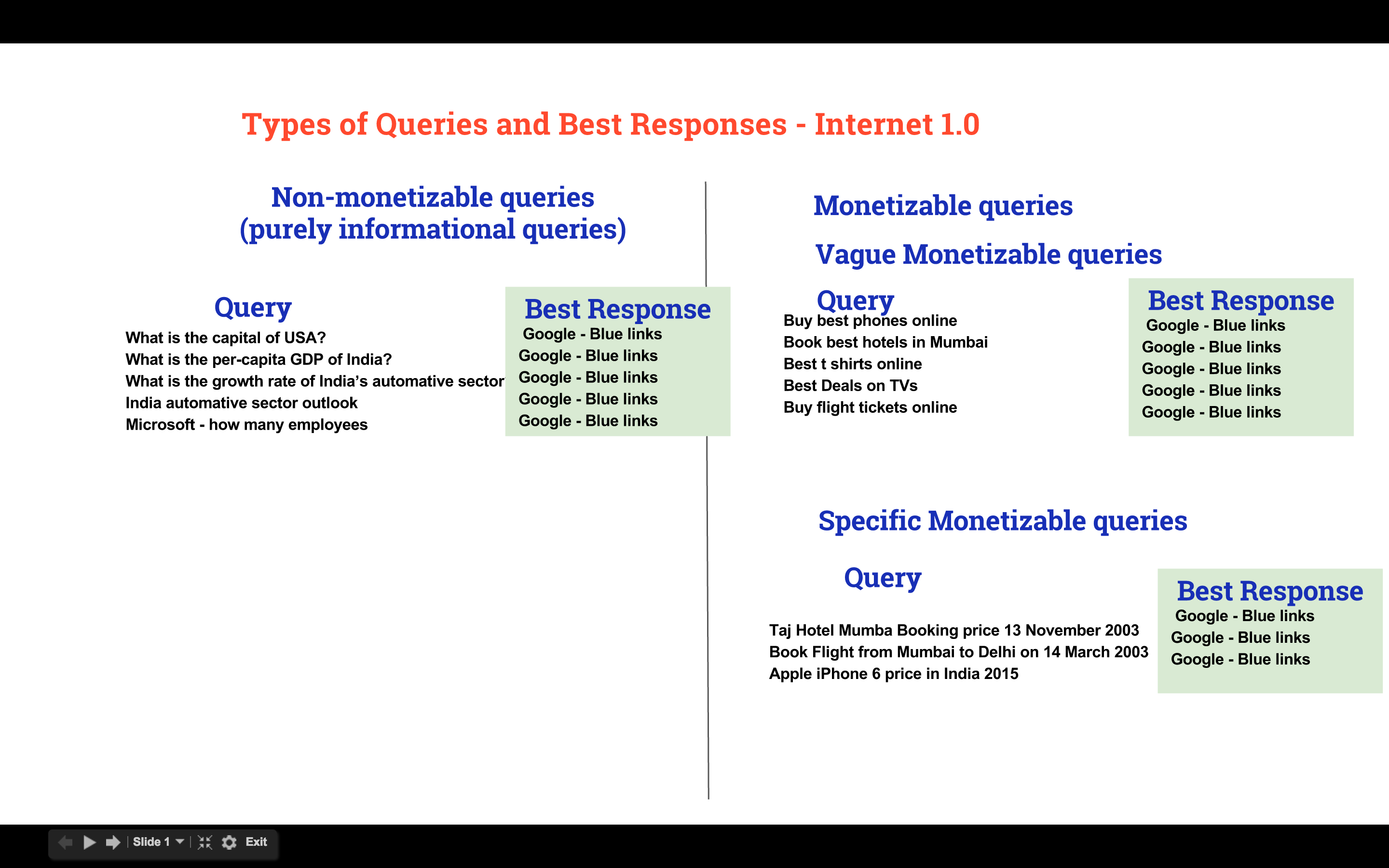

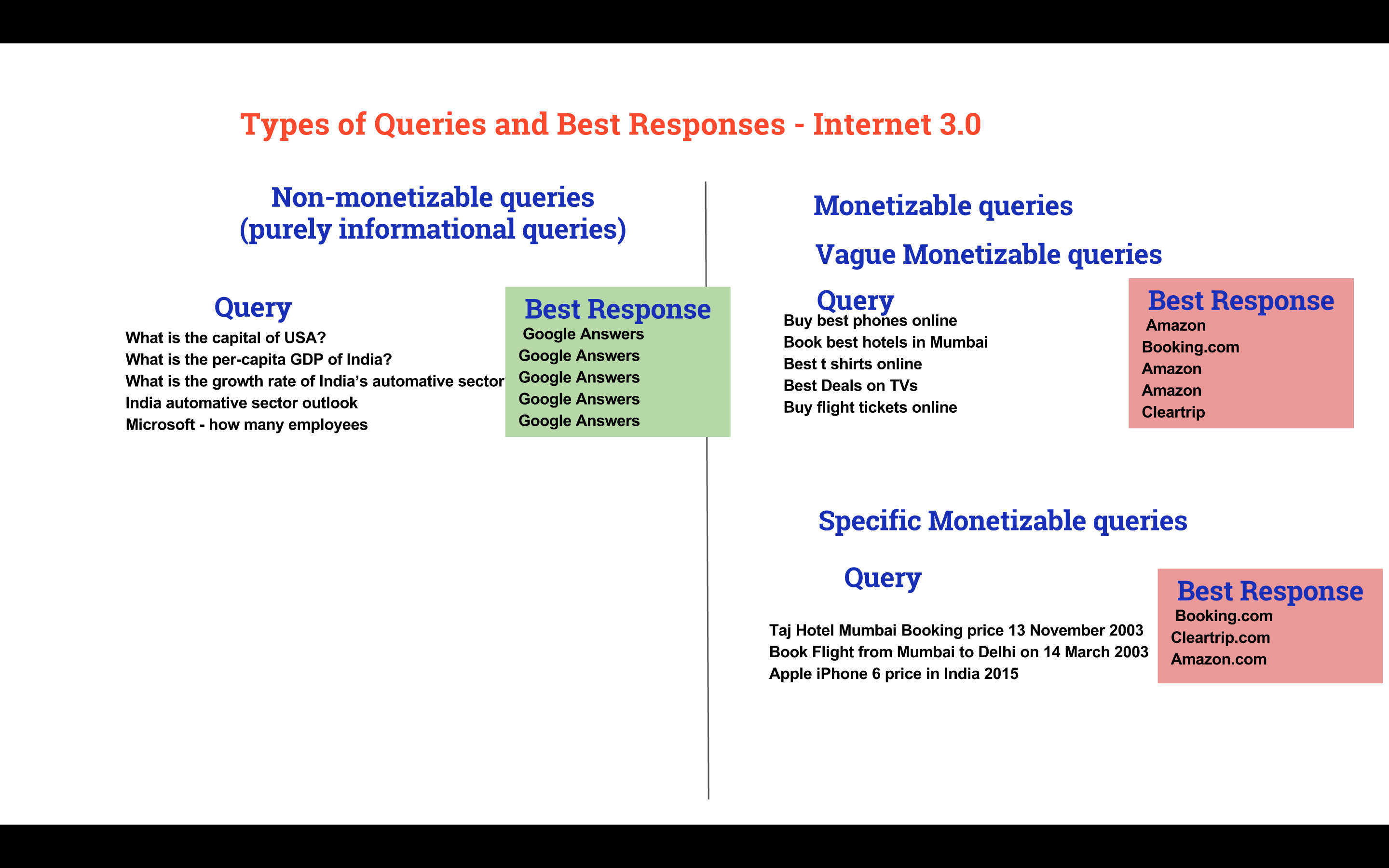

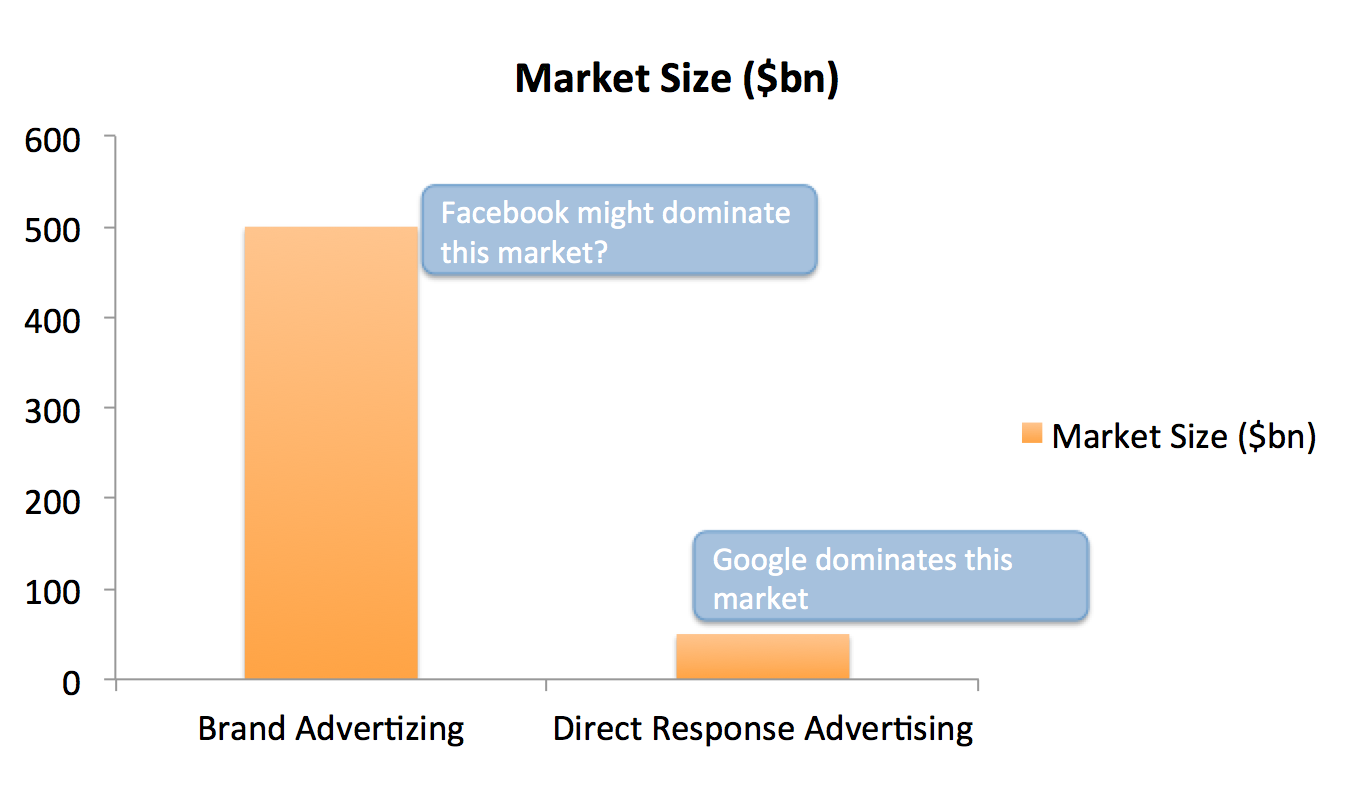

Google may have dethroned Apple as the most valuable company by dint of its financial reporting discipline, but I’d say they should keep the champagne on ice. Industry shifts like transition from web to mobile computing are always fraught with risk I think the jury is still out on whether Google is the company that holds all the aces for the era of mobile computing. Android may have been a defensive masterstroke by Google, but having a safeguard against irrelevance is quite different from having a weapon of dominance. So here’s my take on the major challenges that the company will face going forward.IntroductionI see the company as the sum of two businesses - - a consumer focussed advertising business- An enterprise business (Google for Work, Google Cloud Platform etc)I’ll be mainly writing about the challenges for the consumer business, and will follow it up with a short take on the challenges for the enterprise business. The ChallengesChallenge One - The Internet Matures, Amazon and co grab lion’s share of all the commercial opportunities, Google becomes more like Wikipedia + Yellow Pages for Local businesses.Let’s see the various ways in which we have sought information over the web, or, the full universe of queries.I basically see two broad types of queries1)Monetizable Queries (these can be either specific or vague)1) Non-monetizable queries (a.k.a. Informational queries)Internet 1.0 - In the early days of the internet, Google had the best answers to both types of queries. Also, businesses were still figuring out monetizable opportunities on the internet, and, broadly speaking, the internet was like a huge labyrinth, and Google was the only company with the map to navigate it. Internet 1.0 saw users going to Google for every type of information.Internet 2.0 - The rise of Amazon and the aggregators As the internet matured, aggregators built businesses around specific verticals, realizing that there were profits to be made by offering consumers a customized search experience for specific needs - like flights (Expedia), and hotels (Booking.com) and local businesses (Yelp). Moreover, Amazon morphed into an everything store that sold all manner of goods. All these trends pose varying degrees of threats to Google.Two factors determine whether the user chooses Google or the aggregator/Amazon to do his search. Both these factors can be combined under a single head - the user experience. Since both Google and the aggregator/Amazon can be browsed for free, the user will tend to navigate towards the website that provides a better user experience, i.e. answers his query more effectively. The two factors that govern whether the user goes to Expedia/Zomato/Yelp/Booking.com/Amazon directly, or whether they go via Google, are the following 1) The specificity of the query: For specific queries (i.e. Flights between Mumbai and Delhi on 14-Mar-2016, Apple iPhone 6 Price in India 2016) - the aggregator/Amazon provides a better user experience. That’s one of the reasons why you will find that flight booking sites’ share of direct traffic would be rather high as compared to their search traffic[source: Similarweb stats for Expedia]. On the other hand, in some areas (e.g. local businesses and restaurants), our queries tend to be extremely vague. Another type of vague query is “best smartphones in 2016”. For these vague queries, it is Google that provides the best answers. Therefore, you will find that websites like Zomato, Yelp, rely quite heavily on search traffic[source: SimilarWeb stats for Zomato, Yelp, TripAdvisor].2) The brand awareness about the aggregator/Amazon: This is what I mean by “maturing of the internet”. As the consumers who are online transact with greater regularity, they will become aware of and get accustomed to the user experience of the aggregator. E.g. - a first time internet user is likely to search for flight tickets on Google, and then possibly follow the link to Expedia. A regular internet user will probably go straight to Expedia.Conclusion of Internet 2.0: As a result of Internet 2.0, I believe, the universe of queries for which experienced internet users start with Google, has decreased. We now go to Google mostly for informational queries, and vague monetizable queries. I hypothesize, that aggregators and Amazon may have made dent on Google’s revenues by establishing themselves as gateways for specific needs of users. This dent may not be visible on Google’s revenue reports, because of three reasons1) Broader growth in internet usage - both, in number of users and in time spent online, i.e. the pie for overall online transactions growing extremely fast - allowing Google’s revenues to grow unabated even if it has a lower share of total2) Google gaining revenues from aggregators outbidding each other for traffic from Google - because of their low brand awareness.3) Google gaining revenues because of extremely high proportion of vague queries. Internet 3.0- The likes of Amazon etc will use advertising (integrated marketing campaigns), email-marketing, referral programs, blogs, loyalty programs and every other trick in the book to wean themselves away from Google as a traffic source. How this will play out is anyone’s guess, but I see Google losing out a bit on horizontal e-commerce (i.e. people will stop searching “best smartphones to buy” and instead go straight to Amazon). I think Google will continue to remain strong in local businesses/restaurants and holidays. The doom scenario is, Google becoming Wikipedia + Local business Search + Vague Queries Search.Search : Web :: Messaging : MobileSearch was the killer app for the desktop web. Not so much so for mobile - because it is difficult to write and type, on such a small screen. Speech recognition, although it has produced impressive results, is still some distance away from mass adoption. Technologies like SwiftKey have helped ease the pain of typing, but all in all it looks as if the dominant model on Mobile usage may not be search after all. It may not be the various apps in walled gardens, or the notifications centre either.The most critical activity we do with mobile phones is to communicate. Therefore, the messaging app, which already has a lot of core usage, seems like a good candidate to become a container for all kinds of ancillary services. This is already happening in China - where people book cabs, tickets, buy stuff, make payments etc through WeChat. The reason it works is because Messaging is anyway the most important activity on the phone and it turns the user into a captive audience for all sorts of other distractions.If this is the way forward, it could unlock a new set of experiences and business models - either advertising-based or commission-based - that are activated through the messaging app. This should be of concern to Google - because the Hangouts app is not really as good as Whatsapp or FB messenger. All in all, FB seems to have benefited more than Google from the shift to mobile. The challenge from Facebook in Brand advertisingThere are broadly two types of advertising - direct response advertising and brand advertising. Direct response advertising is about giving people relevant information and generating an immediate sale - it’s fairly transactional and not emotion-based (e.g. - ads on the Google Search Results page - prompting you to buy a phone from Flipkart - when you search “best smartphones 2016” - can be considered as direct response ads). Brand advertising, on the other hand, is about manipulating people’s emotions and creating an awareness and affinity for your product. It is not aimed at generating an immediate sale (e.g. a Youtube Video advertisement about Coca-Cola, can be considered as brand advertising). Any guesses as to how big are the two markets?The direct response advertising market is about $ 50 bn, whereas brand advertising market is worth $500 bn (the difference is because, with direct response advertising, advertisers are making you buy their product once, whereas, with brand advertising, they are trying to make you buy their product every time). Google dominates the market for direct response advertising. Brand Advertising, on the other hand, is right now mostly still spent on Television commercials, it will slowly move online.And when it does, I believe Facebook and not Google would dominate that market. The outcome that brands are trying to achieve, involves the manipulation of your emotions and insecurities, at scale, and Facebook is where this happens with maximum impact, not Youtube. Youtube may be where they are uploaded, but Facebook is where they will go viral, and Facebook is where the conversations will happen, with real people. As such, there is a good chance that the majority of brand advertising dollars may go to Facebook.Google Apps for Work and Google Cloud PlatformGoogle’s corporate offerings can be summed up under two headings - (1) Google Apps for Work and (2) Google Cloud Platform. There is a fantastic opportunity here to combine the two offerings and position Google as a one-stop-shop for all the corporate IT needs of customers. Which customers? This is the problematic question for Google. One way to segment the customers, is by customers’ willingness to pay, and going by that, I find two segments.

High willingness to pay - Large corporates fall under this bucket, and this category is likely to be the more receptive to cross-selling and upselling propositions. The catch is that they would probably want solutions at their fingertips - i.e highly advanced features and fully customised solutions.

Low willingness to pay - Startups, SMEs, government/education sector would fall under this bucket. These companies look at specific IT needs in isolation (limiting the opportunities to cross-sell and upsell), and they don’t really need the advanced features.

Google’s dilemma on Google Docs, Slides and Sheets I believe Google Docs, Slides and Sheets have the unmistakable imprint of Google as an organization - specifically its focus on excellence in product scalability. Google Search is the perfect example of a scalable product. The same rectangular search box works for every kind of user, for every kind of search query. This obsession with scalability is probably ingrained in the organization and in everything they do. If you build Google Docs, Slides and Sheets with this philosophy, there are two routes you can take - Route one: Build every possible feature for every possible user along the entire spectrum of basic to advanced users. (This is what Microsoft has done with its productivity apps). The process for building this way requires market research, requirements gathering and custom software development, i.e. the process is completely non-scalable, although the end result is a single product that is useful for all users.Route Two: Build the basic feature set that is guaranteed to be used by all users, and eschew the advanced features. The process for building this way is all about web scalability - that Google is so good at.Naturally, Google seems to have taken Route Two. The problem with taking this route is that the resulting product will appeal mostly to consumers (individual users) who would want it for free and only to those corporates with low willingness to pay. If they want to move the sales needle, it would require selling to large corporates, which would require building those advanced features which would appeal to them, for which said corporates would begin to open their purse strings. Now, custom software development, requirements gathering, market research etc. are not probably the Googley way of doing things, but it does look to be the right way forward for this part of the company. Giving the sales guys a seat on the product development table, and maybe, acquiring or partnering with companies that are already entrenched in the corporate space is probably how Google would be moving forward.AWS has deeper pockets than meets the eyeA final point I wanted to make, is that Amazon may have only $2bn in the bank, as compared to Google’s $73 bn and Microsoft’s $92 bn. This seems to give Google and Microsoft significant leeway in a price war with AWS for cloud computing. The only point to note here is that AWS is operating at significant scale, compared to competitors. This gives its money a multiplier effect. Cost of serving a customer would be much lower for AWS, and hence, for a given amount of money, it can buy many more customers than its competitors. Competing on features as well as price, rather than just price, may be the right way forward.

{kind=link}

{kind=link}

{kind=link}

{kind=link}