My fascination with flying...

Flying has always fascinated me. It so amazing how one can defy gravity and be so high up in the sky that huge cities start looking like doll houses when you peer down at them. An integral part of realizing this fascination, i.e. making me ‘fly’ is the airline companies that possess all those huge planes with snout-like fronts and tripod-like tails scheduled to zip-zap between destinations. Of late the airline industry is under everybody's radar (post the now infamous Malaysian-Airline-gone-missing case) and many commentators in the white and pink pages of esteemed newspapers have gone on to argue how the oh-so loss making airline firms with their lax security standards, ill-trained pilots and what not are playing with the lives of their passengers.

So this set my mind churning. Despite practically everyone ‘going by air’ and airports turning into railways stations due to the frequency and extremely low prices of air travelling, firms in this industry still don’t make a profit. Now I have had the distinction of studying Economics at the undergraduate level (although I don’t know how much I remember :p), so I thought now might be a good time to use my limited analytical know-how and enlighten the world with it . So, looking at airlines as an industry, I started with figuring out how much control do they have over their costs and revenues.

The airlines industry - cost structure

Airlines have little control over their cost structure - most of the cost components are either totally beyond control (fuel prices) or controlled by monopoly/oligopoly suppliers (aircraft purchase, airport usage fees etc)

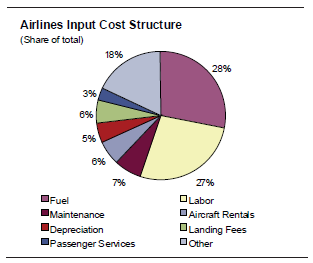

Major costs in this sector are costs of Aero-turbine fuel, costs of renting aircraft and fees to Airport Authorities (for landing, parking and usage of the airport). The cost of ATF is in the hands of major oil suppliers. With suppliers being limited in number and oil prices fluctuating on a daily basis, it gives airline firms zero bargaining power. Second, the cost of renting an aircraft is controlled by the owners. Even in this industry, demand is generally in excess of a rather inelastic supply. Thus, the price is sticky upwards and not in control of the firms in the airlines industry. Third, the fixed costs associated with airport usage is decided the governing authority (for India, the Airports Authority of India)-again, a cost that is totally not in their control and over which they have zero bargaining power.

The following graph depicts the major operating expenses of the airlines industry:

[Graph courtesy: http://seekingalpha.com/article/928911-flying-below-the-clouds-a-common-sense-analysis-of-airline-investing-opportunities]

It is notable that most of these are expenses over which Airline firms have little to no bargaining power and are governed by monopolies or oligopolies, causing a further escalation in prices (since they charge prices higher than those under perfect competition). Another pertinent example is the purchase of aircraft - this market is also dominated by two major suppliers - Boeing and Airbus. In this case too, airlines have limited control over their costs.

The airlines industry - revenues

Price-sensitive demand, and extremely high competition

Now coming to revenues, airlines as an industry is characterized by multiple players who are looking forward to grab a share of the existing market from each other by price undercutting. Also, the demand is highly sensitive to macro-economic factors like global economic conditions (a reduced disposable income would lead to decreased expenditures across the board), geopolitical situations (would you want to fly to a country hit by civil strife?), etc.

Is the industry better suited to be an oligopoly?

Thus, we are looking at an industry that cannot predict either its costs or its revenues with any degree of certainty. Therefore, it is only obvious that such firms will not be on your top performing list. This is a unique business since not only are its fixed costs high but its variable (operational costs) are also high and while the total cost of operation is huge, the marginal cost is negligible (the cost of putting another passenger on a flight that is anyway scheduled to fly is negligible as compared to the total cost of operating that flight). Thus, it is no surprise that most of these firms struggle to become profitable. I guess, this industry is more suitable for monopoly or oligopoly market structures, so that the players may be able to obtain super-normal profits and reduce the uncertainty and leanness in at least their revenues, if not their costs. Only time will tell where this industry is headed and in the meanwhile, we can only hope that nothing like the Malaysian Airline incident happens again.

Akriti Gupta, BM class of 2015 student at XLRI Jamshedpur. She is a writer by hobby, a speaker by vocation, a painter on whim and a student by compulsion. She hails from Delhi-NCR and has been to Delhi Public School, R K Puram and Jesus and Mary College, Delhi University to study about..well..things that she doesn’t remember any longer.

If you want to read more from her

Samarthya-The counselling initiative of budding managers at XLRI

Follow Akriti at InsideIIM at akritigupta.insideiim.com