How to plan your finances and invest money in India in your 20s - A detailed step-by-step guide. So I have been meaning to write about this for 10 years now. It is the one thing on which I have advised countless people for over a decade now. This list of people includes CEOs, business consultants, young entrepreneurs and even some of my financial advisors. I do not claim that this is the best or the only way to invest – simply that this is how I am investing and how I would advise anybody who asks me for advice to invest. The rest is up to you.

First things first, Why I am qualified to write this?

I began my career with one of India’s best wealth management outfits in 2001. I’ve seen the ups and downs of pretty much every one of the last few cycles in India – the don’t touch stocks period after the 2000 crash, India will rule the world period from 2003 to 2008, the great financial crash of 2008 (I was actually sitting in the Lehman office in NYC when Lehman imploded) and the rejuvenation of markets from 2011 to 2016. There’s no investment scam that I haven’t seen and no get-rich-quick idea I haven’t evaluated (both wrongly and rightly). I’ve started my own company and sold it. I’ve traded public equity stocks in the stock market and now invest in private companies for a living. Most importantly, I’ve made some decent investments through this period and have a decent track record. So if you find the financial world too complicated, maybe this series would be of help to you.

Simply put, I began my career in 2000 and quit my job in 2011. From 2011, I ran my own company for 5 years during which period I invested into the business and did not withdraw a single paisa from the business until I sold it in 2016. So basically, in 10 years of working, I managed to save enough to retire comfortably and maintain a good lifestyle for myself and my family – and we still did everything we did when I was working as when I was a “poor” entrepreneur. To me, that is something that I wanted to be able to do since the day I began my career. If that is something that works for you, please feel free to follow this list. If it doesn’t, contact your bank relationship manager or stock broker and he will undoubtedly be better qualified and happier (and better-remunerated) to help you.

Enhance Your Earning Potential. Advance Your Career.

Join the Klub of India's Top Professionals

We are excited to inform you that we are kickstarting our live industry sessions at Klub AltUni with Kenneth Serrao on the 17th of July! The topic is 'Investing In Brands'. If you find this article to be useful, you may also be interested in interacting with Kenneth to learn more about investing! At Klub AltUni, we are hosting weekly sessions with industry stalwarts, and offering 1-on-1 personalised career guidance and exclusive job opportunities! Join the Klub here!

So without much ado, here is what I do (and advice you to do). This is obviously a slightly long post, so I will be putting it up in several parts. The whole piece consists of 4 parts.

- Know your investment amount and the horizon

- Choose what to invest in

- Rebalance your portfolio – or not

- Know what to avoid.

Since most of my readers are super-intelligent, I will just present the quick and dirty summary here. I will explain each of these 4 parts in detail in the next four posts this week (for explanations and detailed reasoning on why I suggest these, read the follow-up posts)

- Knowing Your investment amount and the horizon – how much money do you have to invest and with what horizon. How do you decide that?

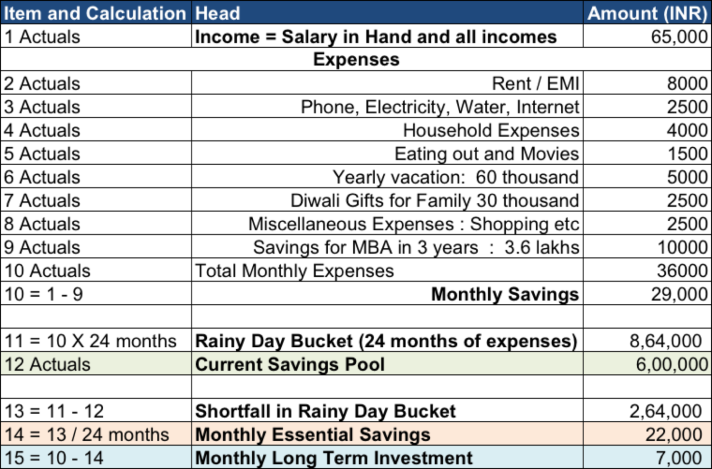

- Know your monthly income and expenses. Account for one-off expenses like vacations as regular expenses and add these up over a year. Since you know what comes into your bank account regularly, once you have understood your expenses, this should be simple enough.

- Put away 2 years of expenses in a Rainy Day Bucket. While doing this exercise, think about your expenses and see if there are any expenses you could reduce. Your investment mantra has to be “SPEND LESS, INVEST MORE”.

- Identify significant planned expenses in the next 3-5 years of your life. These are the usual goals and milestones that you are asked to identify by all advisors. Children College education, Buying a house, MBA degree you yourself want to do in a few years after saving from your current job etc.

- Here is an illustration showing how to calculate this with some sample numbers. All numbers are in Indian Rupees.

And so you now know all that you need to know in order to start picking your investments. 1. Current Pool (Rs. 6,00,000 in example above) 2. Essential Monthly Savings for Rainy Day and 3-5 year needs (Rs. 22,000 in the example above) and 3. Monthly Long-Term Investment Amount (Rs. 7,000 in the example above). Once you have established these 3 numbers, you are done and know your balance sheet well enough. You are now ready for the next step.

- Choosing what to Invest in – Provident Fund, Fixed Deposits, Mutual Funds, Stocks, Property, Gold, Real Estate etc. There are so many options. Choosing which investment to make is now an important decision for you to make. This is largely a function of the time horizon you have and the kind of returns you should make. For me, I keep this reasonably simple. I shall explain what I do below.

- Fixed income for the Rainy Day Bucket. This is important. You cannot afford to take any risk on this amount since you will not have the time to recover in case you do make a loss on these investments. Hence this investment amount has to be kept in the safest and easily accessible investments. Historically, this used to be simple – you just had Fixed Deposits to do this. Nowadays, there are a few more options, especially liquid funds for money that you might need any given day.

- You can put about 50% of this money in Fixed Deposits with reputable banks (avoid co-operative banks and stick to the largest, safest banks here). Try and match the duration of the Fixed Deposits with your known expenses (In the example above, you could choose 3-year fixed deposits to match the MBA need).

- For the balance 50% of the money that you could require any given day, put it into a category of Mutual Funds called Liquid Funds. Liquid Funds are safe and almost guaranteed to not be negative on any given day. Choose liquid funds from any reputable mutual fund house for this – Franklin Templeton, ICICI, HDFC, SBI and Reliance work for me. This money is available for you on any given day and gives you returns that are almost similar to Fixed Deposits with greater liquidity.

- Invest in PPF – the best investment in India. The PPF is simply put the best investment you can make in India. In actual numbers from the last decade, the PPF on the average gave you 9% returns (slightly higher than Fixed Deposits) with 3 significant benefits – PPF investments are exempt from income tax (so if you invest 1.5 lakhs in PPF you will get a tax exemption for the same in your annual income tax), PPF investments also are exempt from income tax when you withdraw the amount after 15 years and the returns are also exempted from income tax. These three benefits (EEE status) basically mean that you are earning a risk-free rate of around 11%-13% (depending on the tax bracket you fall in). This is almost equal to the long-term return of stocks (or any other investment option in India). The only catch is that there is a limit on this investment. You cannot withdraw it before you complete 15 years and you cannot invest more than 1.5 lakhs per person in this scheme. Here is how you should invest in this particular investment on a step-by-step basis.

- Maximise your PPF investment to the limit possible. Fill up the 1.5 lakhs per year limit for all your family members (this includes minors). Until you exhaust this PPF limit, do not even look at anything else

- If you have a daughter, maximise the Sukanya Samriddhi scheme investment also (same as PPF with similar limits and benefits but only available in the name of a girl child if you have one).

- For a family of 2 parents and a kid, this limit basically becomes 1.5 lakhs x 3 = 4.5 lakhs a year. If the kid happens to be a daughter, then the total limit rises to 6 lakhs per year. Until you have exhausted this 6 lakhs per year limit, do not even look at anything else.

- Most importantly, almost no advisor recommends this because it does not give much incentive to distribute PPF (no fat commissions). So you will have to do this for yourself. Go ahead and max out your PPF investments. You can do this through any bank or through the post office. I find it simplest to do this through my mobile banking app.

- Buy a medical insurance and term insurance to cover your life. Life is uncertain. Plan to save your family from any such uncertainty. Buy a simple term insurance from a reputed insurer (my personal preference is ICICI). The sum assured should be about 20 times your annual salary to ensure that your family is not at all impacted by anything that happens to you. In addition to this, buy a medical insurance to cover any unplanned medical expenses. Again, my preferred insurer is ICICI Lombard (they have great customer service) but you can choose any other insurer that you are comfortable with. If it helps, understand that IRDA (the Insurance Regulator for India) has made rules that make it virtually impossible for any insurer to go bankrupt. So, your choice of an insurer should just be one that covers the hospital that you usually go to. Enough said on this topic. Actually no, one last thing. DO NOT BUY A ULIP or any other insurance-linked product. Buy a simple term insurance and a simple medical insurance. For investments, buy investment products. More on this in later posts, but that is all you need to know.

- Buy a house once you are settled (and buy only one house) On this one, the simple advice I have is – buy a house where you will eventually settle down. And buy a house that is a little bit of a stretch in terms of expense as well as size. Account for your family and lifestyle (as well as your income) to grow and then go for it. And lastly, buy only one house.

- Why stretch yourself? Because it is very very difficult to buy and sell a house. Apart from the very high costs, brokerage, taxes etc, it is such a high-value investment that you will not be able to manage the cost of two houses if you upgrade (unlike say a mobile phone or a car where you can buy another and sell the first later). Moreover, every time you buy or sell a house, you will also spend a considerable amount on doing up the new place. So buy once and buy something that will last you a lifetime. If you cannot afford it, wait until you can and then buy something that works.

- Why buy only one house? Houses are illiquid and not particularly good investments over a complete cycle. Unless you are buying them when rental yields are comparable to EMIs (and it happens frequently like between 2000-2004 India or between 2009-2014 US). But for your primary house, you don’t need to worry about yields and prices and complicated things like that. Just buy something that works for you for a considerable time and which you can afford.

- To summarise, buy a house you can grow old in as soon as you are settled enough to know that you will grow old in a particular place or job and can afford it. The typical rule of thumb is to buy it with 3-5 years salary. This rule of thumb is based on simple logic. No matter what happens, you have 2 years of a rainy day fund. You have current visibility on your job for the next 1 to 3 years. So no matter what happens, even if you lose your job and take 6-9 months to find a new job, you are comfortably able to manage your EMIs. So stick to that thumb rule and you should be in good shape. And if you end up getting promoted or making a fat bonus in a given year, prepay your house loans a bit and reduce your outstanding loan. The sooner you get the loan out of your system, the better for you.

- One last thing about buying a house. Apart from the peace of mind that owning a house gives and the tax break that you get for paying EMIs, there is also the behavioural effect of forcing people to save more. I know many many people who started forcibly saving when they had EMIs and were forced to cut down on discretionary spending to afford their EMIs. This is a very real factor that should not be ignored. Ideally, you should cut down on your discretionary spending even if you do not own a house. As mentioned previously, “Spend Less, Invest More”

- Buy Stocks with the rest of your money. For the rest of your investment portfolio, my view is simple. India is one of the best investment destinations for global investors.

- Indian stocks are at a cannot-go-wrong, once-in-a-decade kind of investment opportunity. There, I’ve said it. Either you agree or you don’t. With growth in most major markets severely challenged and the end of a multi-decade bull market in bonds, there is virtually no way global investors can avoid India.Even in India, less than 1% of the population owns stocks. Everyone has fixed deposits and real estate portfolios. As with every developed economy, eventually, you should expect this proportion to rise significantly. This, in essence, provides a floor to how much markets can fall in India. The monthly SIP flows over the last few years now have proven that Indians investing in stocks is a trend that is a structural one. Benefit from it and get invested as soon as you can prudently is all I will say.

- You can choose how you want to do this. The simplest and can’t go wrong approach is to do Mutual Fund SIPs. Choose 5 large-cap funds across 5 different fund houses of repute – Franklin Templeton, ICICI, HDFC, Reliance and SBI work for me. Pick any others that you are comfortable with. As always, don’t over-complicate this.

- If you understand the stock market at a very basic level, choose stocks yourself. This saves you about 2%-3% a year which is about 15% of your long-term returns of 10-15% a year on stocks. As you do this for a longer and longer time, you will get pretty good at it.

- Investing in private companies through angel investments, seed investments, venture capital, private equity etc. Across the world, this remains one of the most high-risk-high-return investments you can make. Since so many people ask about this, here is my take.

- If you are investing in a private business, ensure it is a profitable small business with a person who really knows the business and is a god in that space. Moreover, ensure that he/she is totally committed to the business. Business is real hard and many things can go wrong in the short run. Find someone who is in it for the long run.

- Ensure you get a really good deal – significantly better than public stocks. I know people who invest in small startups at valuations that are 3-4 times the valuation of large listed comparable companies. That is never going to end well

- At the risk of repeating myself, ensure that there are real profits and real revenues. You are unlikely to know the next Mark Zuckerberg or invest in the next Facebook. Just recognise that basic fact and you will do well for yourself.

- If you are interested and would like to invest in some great, profitable private businesses, I know this great firm that does a fantastic job of it. Go to www.OaksAMC.com if you want to know a bit more. Disclaimer, I work here.

- Look at this aspect of investing as investing in a real business partnership with a businessman as a financial partner. Most people know how to do this. Look for honest businessmen who need a little capital to run a business that is already doing pretty well. This could create some great income opportunities for you in addition to your main income stream. Do this well and it could help you retire early.

- Fixed income for the Rainy Day Bucket. This is important. You cannot afford to take any risk on this amount since you will not have the time to recover in case you do make a loss on these investments. Hence this investment amount has to be kept in the safest and easily accessible investments. Historically, this used to be simple – you just had Fixed Deposits to do this. Nowadays, there are a few more options, especially liquid funds for money that you might need any given day.

- Rebalancing your portfolio. What to sell, how to book profits, what to buy next? The rule on this is simple. Be Lazy. Do as little as possible. If you focus on getting your investments right the first time – and broadly right is enough, then you don’t need to do too much.

- Never rebalance your portfolio because an investment you made is up 300% (or some such figure) and hence has become 20% of your overall portfolio. Imagine people selling Infosys after the stock went up 100 times. They would have missed out on another 100 times their returns. Ride your winners.

- The exception to this is when you discover that a particular investment of yours is a particularly bad investment. Say you discover that the management of a company whose stock you own is not particularly scrupulous or the key promoter of a company you own is in particularly bad health. Or you discover that a company has started to take on significant levels of debt in order to grow its business that is otherwise degrowing or becoming a lower and lower margin business. Think hard about it but cut your losses if the basic facts about it change. And whatever happens, avoid throwing good money after bad.

- List of things to avoid like you avoid a person with an infectious cold – sometimes I feel this list is the most important list of all since most people understand the first 3.

- The next great asset class – whatever it is. This includes all and more of the following type of investments – bitcoin, namecoin (yes that’s a real cryptocurrency), structured products created by your bank that are too good to be true (and indeed they always are), agricultural commodity derivatives, range accrual products, art funds, real estate funds and other such exotic products. As mentioned twice previously, don’t overcomplicate your investment portfolio. Simply put, stocks are the next great asset class for India. Stick to them.

Phew! That’s long enough already. Wish you a significantly more prosperous life.

Note From The Editor -> We are extremely excited to start Klub AltUni on the 17th of July with Kenneth! Here's your chance to improve your payscale, get promoted, make career transitions and expand the quality of your professional network! Join the Klub now!

Listen To The Podcast Here!

***

About the Author:

Kenneth is an alumnus of IIM-A (Cultural Secretary, 1998-2000 batch). Prior to his management degree, Ken graduated in Mechanical Engineering from NITK, Suratkal (formerly KREC) in 1998. Kenneth is an Army kid who did his schooling in 9 different cities across India. He is extremely passionate about technology, test cricket and financial markets. View all posts by Kenneth Serrao