'Is India ready to become a cashless economy?' is a question that has recurred frequently as a GD-PI-WAT topic for the last couple of years during the b-school admissions process. To help you answer this question like a pro, in this article, we will investigate various standpoints and derive our own answer to this question!

Are you ready? Let’s go!

First Things First - What is a Cashless Economy?

A cashless economy is a type of economy where all types of monetary transactions are done through digital means like - debit/credit cards, e-wallets, internet banking, electronic fund transfer, mobile payments, and other evolving payment channels. When such an economy thrives, there is little or no scope for hard cash to flow in the economy.

Types Of Cashless Payment Mode

- Plastic Money: The term that is mostly used for hard plastic cards. They come in the form of various cash cards, prepaid cards, store cards, credit cards and debit cards. Out of all the other cards, debit and credit cards are used the most. However, people prefer debit cards because they are considered safer. With credit cards, there is a risk of overspending. Both debit and credit cards can be used to make online and over-the-counter purchases.

- UPI Application: Our mobile numbers are registered with our banks and linked to our account, and that’s the basis of the Unified Payment Interface (UPI) functionality. This mode helps in sending or receiving money without entering bank-related info. UPI applications that are currently popular include BHIM, PhonePe, Google Pay, ICICI Pocket, and SBI Pay, etc.

- Mobile Wallets: In this, you need to load money into your e-wallet, and use it wherever it is accepted. The most popular mobile wallet is PayTM.

- NEFT & RTGS: National Electronic Fund Transfer and Real-Time Gross Settlement are electronic payment systems that help in seamless fund transfer between two bank accounts. Both facilities are maintained by the RBI (Reserve Bank of India) and can be used to transfer money within India.

- IMPS: IMPS or Immediate Payment Service, is a service initiated by National Payments Corporation of India (NPCI) where users need to register for both mobile and internet banking. One can send or receive 24*7, instantly and with no cut-off time. It’s done using receivers like - MMID (Mobile Money Identifier), IFSC code or bank account number.

- USSD: Unstructured Supplementary Service Data is a cashless option that works without internet access. It’s a kind of mobile banking facility where you dial *99# to use the service. It uses MMID with mobile number or IFSC code with the account number to complete the transaction.

- QR Codes: It's an extension of mobile wallet service. One needs to simply scan the code of the merchant in order to complete the transaction. There needs to be a smart device, a camera and a scanning facility.

- Net Banking: It’s an alternative to using debit or credit card. Users need to login to a net banking account for approving a payment. One can do net-banking even when their debit card is misplaced. This can be done for utility payments, goods purchase, services online, or to send and receive money.

Sweden - The Cashless Society | A Case In Point

While the world is still ruled by cash, there are pockets of places that are moving away from cash. Currently, Sweden comes in the top when it comes to embracing digital payments. If this continues, Sweden could effectively go cashless by 2023 and may gain the title of the “world's first cashless society”. This means, by 2023 Sweden might no longer accept cash as a means of payment.

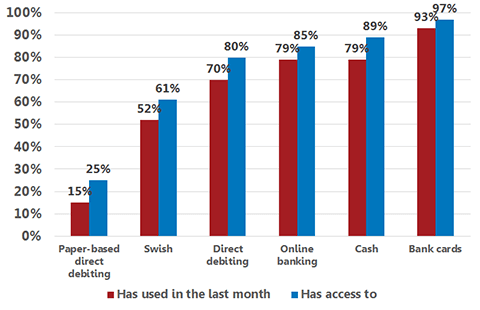

Electronic payment modes such as bank cards and Swish (a Swedish mobile payment system) are the popular means of transaction in Sweden. It seems like Swedes no longer carry cash.

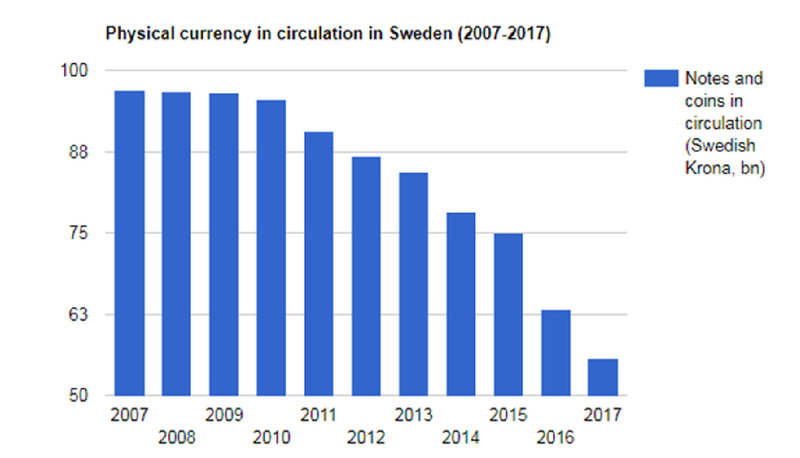

Today, cash represents only 1% of the Gross Domestic Product (GDP) in the Scandinavian country, and the number of cash withdrawals is declining with the passing of every year. Usage of cards keeps increasing every year. Look at the two graphs below. They illustrate both the phenomena perfectly.

Graph 1: Currency circulation In Sweden (2007 - 2017)

Source: Riks Bank

Graph 2: Types of Transactions in Sweden (2016): Use v/s Transaction

Source: Sveriges Riksbank

What are the conditions that are leading to this trend?

- Early digitization of the country: Adoption of payment cards in the Swedish community started way before in the 1950s. Bank accounts started getting digitized in the 1960s. Such a trend along with robust internet infrastructure lead to the adoption of internet banking in the country in the mid-1990s. In the early 2000s, the central bank started outsourcing its printing and distribution. The bank didn’t see cash as its core business any more. Funnily, during that time there was a spate of robberies. This resulted in various organizations like bank employees, cab drivers, bus drivers, etc others pushing for a cash-free society. Other than that, initiatives like governmental steps to abolish black-market government, tax deductions, etc led to a dramatic drop in the need for cash.

- Popular mobile payment app: Swish is Sweden’s Payment App that was launched in 2012. The idea was to build a mobile platform that is instantaneous and simple for customers. It was introduced by a group of six Swedish banks along with the central bank. The app is close to becoming a standard for mobile payments in the country.

- Internet Infrastructure and security: Sweden is extremely fast at the adoption of internet technologies as most of it is subsidized by the government. In future, it is predicted that the internet payments will pick up the retail area, and will probably take over card payments (currently the most common way of payment). The country already has 100% mobile coverage already. Swedes are quick at adopting new technologies and are acceptable when there are changes in payment systems. In return, governments provide top-notch data security.

- Legal framework: Sweden has an interesting legal framework. In Sweden, when a coffee store puts a sign out of his/her shop saying “it does not accept cash”, and the customer still goes to the shop to drink coffee, then both merchant and customer have entered a contract that they don’t accept cash. Even if cash is a legal tender in Sweden, contract laws (like the one between the coffee shopkeeper and the customer) have higher precedence over banking and payment laws. This is one of the big reasons why Sweden is more cashless compared to other countries is because of its legal framework.

- Cultural factors: In many countries, cash notes are an important part of culture and society. For example, America has a culture of tipping, that’s not the case with Sweden. Many cultures have a religious, social, psychological and emotional connection to “cash”, but that may not be the case with Sweden. Hence, it is easier for the country to get cashless.

- e-Krona: Sweden’s Central bank has already started its digital currency initiative, e-krona. The pilot scheme was started in 2019 and will be implemented in the country by 2021.

How Close Is India To Becoming A Cashless Society?

The mention of ‘cashless society’ started when the government decided to ban 85% of the currency in circulation in November 2016. Even though seen as an isolated event, demonetization forced many Indian’s go cashless. However, the real deal started a few months prior to the cash bank and it was the innovation of UPI (Unified Payment System).

Even though the term might seem a little mouthful, the idea is pretty simple. One smartphone user and customer of Bank A can request or initiate a payment to another owner of Bank B. Neither party needs to know anything more than each other’s mobile number or a virtual ID. In this case, India was much ahead of many Asian countries like Singapore and China. The introduction of UPI and demonetization also helped in an increase in internet users in India. In 2016 it was 450 million internet users, a number expected to touch 700 million by 2020.

However, India is not ready to be cashless.

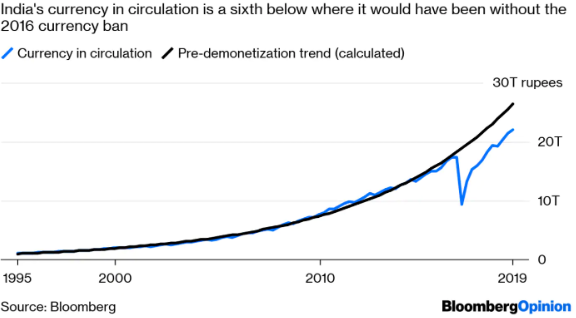

Source: Washington Post

- Cash is still the king: Despite so much drama, India is still lagging in the cashless economy race. Cash is still a king in India. According to Rahul Chari, the co-founder and CTO of PhonePe, India is still at a nascent stage when it comes to being cashless and taking full advantage of the fintech revolution and there’s a lot of scopes to do more in that space. Look at the above graph to understand the current currency circulation situation in India.

- Adoption rate: In an adoption and penetration perspective, it is still a long way to go. The Indian market is still cash-heavy and India is just at the tip of the iceberg. Digital payment mode has only penetrated into the Urban cities.

- Internet Connection: The internet connection in India is very sporadic. 4G is still not available everywhere. Many digital payment companies like PhonePe, G Pay etc are trying to figure with payment alternatives for 2G networks, but that may take some time.

- Public Distrust: If we understood one thing about Sweden’s cashless society experience, it will be “trust of people over the government, banks, payment app companies is very important for a society to go cashless”. Many Indian citizens still distrust cashless payment modes. There are a growing number of fraud cases where people call and SMS people as customer care representatives to get delicate information regarding their bank account and extract money out of people.

- Digital Illiteracy: A recent report by the Digital Empowerment Foundation indicates that 30% of our population lags on basic literacy and thrice that for digital literacy. The gap in illiteracy is much more if you consider the rural and urban places in the country. Even the economic ability to possess a digital device, let alone having a bank account is a struggle for many people who live below the poverty line (which comprises the 22% of the total population).

- Unnecessary charges on online transactions: Banks and merchants charge 1-2% on the total amount of transaction when they offer an online payment facility. This cost of making the transaction increases the burden of the customer.

- A limited number of bank accounts: Around 191 million Indians over the age of 15 are still without bank accounts. Most of the time it is just one account per family, which limits the number of cards people can have per family.

- Political Unrest: In recent times states like Jammu and Kashmir, North-eastern states, etc face crackdown due to political reasons and the first thing that gets blocked is the internet. Ins such circumstances cashless transactions like usage of the card, e-wallet, UPI becomes impossible.

Opinion

India is not ready to fully embrace a cashless economy. Perhaps the country can try to implement the concept of a cashless economy on a smaller scale and excel at that first. Once the concept gains broader acceptance, it may well be easier to adopt it on a larger scale. For now, a cashless society is a distant dream but a less-cash society is still a possibility.

Some Questions You May Be Asked In Your B-School Personal Interview

- What are the major obstacles in India becoming a cashless economy?

- What do you know about the government's efforts in helping India become a cashless economy? Is the government doing anything at all?

- Can India ever go completely cash-free? Can India's informal sector - the backbone of the country's economy - be able to adopt a cash-free model of transactions?

- Digital money and financial information is susceptible to cybercrime and is not unheard of even today. Why should I, as a middle-class consumer with limited savings, put myself at risk of losing all my money to a computer hacker and instead not just put my money in a bank where I know it'll be safe?

Other Important GD-PI-WAT Topics (check now)

- Coronavirus And Its Impact On Global Economy: A Possible GD-PI-WAT Topic

- Possible Ban On Fairness Cream Ads | Its Effect On Market, Advertising And Society | GD-PI Topic

- Citizenship Amendment Act (CAA)

- Budget 2020 Analysis

- The US-China Trade War Explained

- Iran USA Conflict

- Article 370 And Article 35A

- Venezuela's Oily Hyperinflation Story

- The Zomato-Uber Eats Deal Explained

- Why Should India Be Friends With Its Neighbours?

- All You Need To Know About Air India

- Opting Out Of RCEP - Does India Need To Rethink Its Decision?

- 65 Topics To Help You Crack The WAT Round

References

- Think Tank urges SC to stop trial of WhatsApp Pay

- True Fintech Will Be Seen In India In The Next Five Years: PhonePe Co-founder Rahul Chari

- Constraints of digital literacy in rural India: Only 21.3% of students have access to computers

- India Is Likely To Become The First Digital, Cashless Society

- India Going Cashless Could Be a Model for the World

- Can India really become a cashless society?

- Sweden: How to Live in the World's First Cashless Society

- Sweden: cashless society and digital transformation

- Sweden’s march towards a cashless economy went into reverse

- What can we learn from Sweden, the ultimate cashless society?

- Going Cashless: What Can We Learn from Sweden’s Experience?