Our student team member Aman Jindal reached out to Rakesh Kumar Yadav and Divyanshu Jain to find out more about the problem of Non Performing Assets, a matter of great concern for Indian Banking and Economy. Here they discuss the matter in detail.

A strong functioning banking sector is the very basis of a thriving economy. The banking sector in India has grown tremendously after Independence, particularly after the neo- liberal reforms. The current valuation of the sector is at Rs 115 lakh crore and expected to more than double to Rs 288 lakh crore by 2020. 70 per cent of business is being done by PSU banks.

Given the enormous size of our banking industry, the present Non-Performing assets (NPA) crisis is a matter of great concern for the whole economy. Because of its domino effect, the crash of the banking sector is having a ripple effect on other related sectors. A significant chunk of the money that the banks lend comes from the deposits they receive from the public and the government. Thus, the existing very high levels of NPA in the banking sector, is not only an issue of great worry, but also is a matter of serious economic concern.

What is NPA?

In India, the definition of NPAs have changed over time and is also different for different industries. For Banks, the assets for which the interest has remained unpaid for ninety days are considered as NPAs. In the case of agricultural loans, if the interest and/or the installment or principal is overdue for two harvest seasons; it is declared as an NPA. But, this period should not exceed two years.

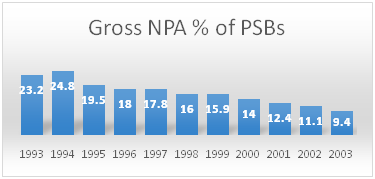

Narasimham Committee and its Efforts at curbing the menace of NPAs

Narasimham committee I in 1991 recommended setting up of Debt Recovery Tribunals which provided an alternative to the banks to recover their dues from defaulters outside the courts.

Narasimham Committee II in 1998 proposed SARFAESI Act which was enacted in 2002 to give banks the authority to attach secured properties of defaulting borrowers.

The recommendations of Narasimham Committee were gradually adopted in the banking sector and it resulted in a sharp decline of NPAs across PSBs. But things have changed dramatically post the global financial crisis of 2008

Global Financial Crisis and the NPA Scenario

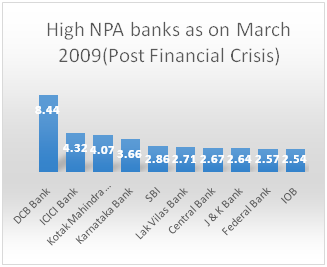

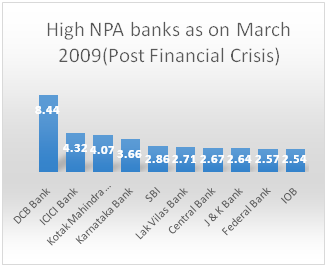

The NPA status of Indian banking sector on September 2008 and one year after that is depicted in the following graph. A startling fact is that in the top ten highest NPA banks, eight slots are acquired by private banks.

What caused this NPA crisis?

Before the financial crisis all the companies were on an expansion spree buoyed by the constant 8-9% GDP growth in the economy. To help this growth, PSBs went on a lending spree and lent to industries like textile and other core sectors like mining and infrastructure etc. Currently, the top five sectors in NPA list constitute 63% of total NPAs. These sectors are textile, mining, steel, infra, aviation in that order. Companies borrowed heavily in the “good times” but unanticipated slowdown in the global markets coupled with policy logjam of UPA II government created Twin Balance sheet problem which led to both the Corporate and Bank Balance Sheets being in a mess.

As these companies were not able to repay their debts, their credit ratings have been downgraded and banks are unwilling to help sick companies because their own balance sheets are stuck with bad debts. This is the result of pro cyclicality in the economy.

Also, the menace of NPA could be far worse than it appears from the outset. Bad loans are hidden in the system through window dressing and manipulative practices.

The impact of NPA

- NPA is a multifaceted problem for the industry as well as the economy because whatever hits the banks sends ripples across the economy.

- Due to a weak corporate bond market, companies are heavily dependent on banks for debt financing. ECB is an alternative but that facility is not conveniently accessible to all companies.

- Banks have to set aside a part of their capital for NPA provisioning, which has a negative impact on earnings.

- Higher provisioning requirements for NPAs has reduced earning capacity of the assets and in turn has negatively impacted their ROA (Return on Assets)

- Capital Adequacy ratios are calculated on top of the Risk Weighed Assets. NPA’s carry risk weight of 100% .Therefore they block capital for maintaining Capital adequacy and can’t be used for productive economic activities.

- NPAs also hurt shareholder’s value creation. People don’t find investing in equities profitable and hence the cost of capital increases significantly for them

- Finally, banks usually have leverage ratio of more than 10 on their balance sheets. This leverage aggravates the problem of NPA. For example, if a bank has 5% NPA and a leverage of 10, it has practically exposed 50% of its loan value to possibility of default. Considering this, RBI is putting in all efforts on cleaning up the balance sheets of PSBs which total to more than 4 lakh crore of NPA, out of the of overall 69 lakh crore loan.

Recent Steps taken to curb this

4R approach

The RBI has given guidelines to control the levels of non- performing assets and reduce institutional default risks that exist. In the recent economic survey RBI proposed a 4R approach i.e. Recognition, Resolution, Recapitalize and Reform to tackle this menace of NPAs.

Indradhanush

The Government has also launched Indradhanush plan, which is a 7 pronged approach to revitalize PSBs.

Conclusion

The giant size of the Indian banking industry demands that we immediately address the NPA menace. It doesn’t only pose a big threat to our macro-economic stability but also projects an anti- investor friendly image of India. Since the problem has multifaceted roots in economic slowdown; worsening business climate; shortage of legal recourse for the companies; and their operational shortcoming at various levels. It also needs to be dealt and addressed at multiple levels. Given the labyrinthine structure of the problem it has rightly received the attention it deserves. Corrective steps supported ably by affirmative actions and a revival of the economy will curb the burgeoning NPAs. Also, we must have long term reformative policies to ensure that the economy does not have to face similar NPA crisis in future.

_______________________

About The Authors:

Rakesh Kumar Yadav And Divyanshu Jain

Rakesh Kumar Yadav is an avid reader with a diverse interest base in areas of Economics and Socio-Polity at large. He is an elected coordinator of Economics and Political Society, a student run interest group at IIM Kozhikode. In his spare time he likes to watch neo-noir western spaghetti.

Divyanshu Jain was a former banker with State Bank of India. Besides a huge interest in Economics, he is a blogger with a special interest in sci-fi and fiction.