Bubble

ˈbʌb(ə)l/

"A term used to refer to a good or fortunate situation that is isolated from reality or unlikely to last"

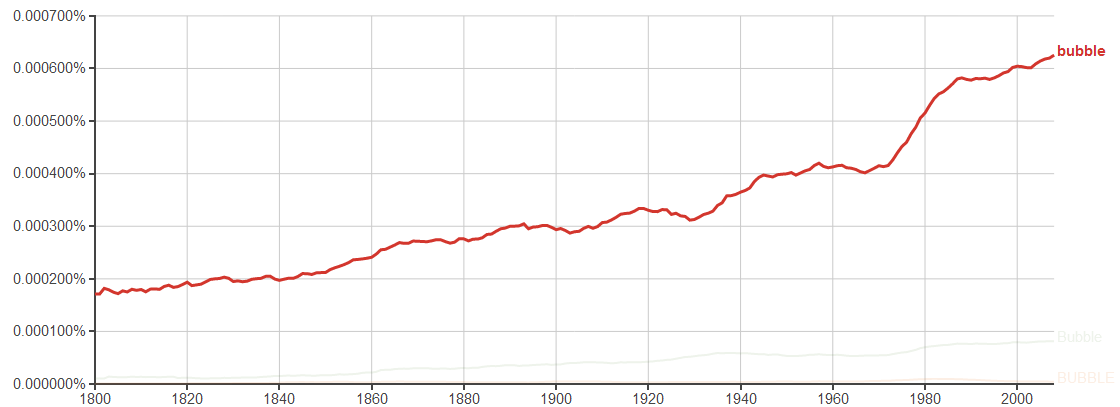

The above graph, sourced from Google Ngram shows how the usage of the word ‘Bubble’ in books and articles (basically in everyday speech) has increased drastically since the 1980s and is on an upward move post the 2000s. This is an indicator of the times we live in. We love inflating expectations, we adore hyped up valuations and worship unreasonably high stock prices. The Y2K bubble, the real estate bubble, the sub-prime crisis are all children that emerged out of this extreme love.

We, at India are catching up this phenomenon, just like we love pouring buckets of ice water over us just because the world did so.

Expectations

There are expectations of a $100 billion firm in the e-commerce industry. There are investors lined up to pour money into their coffers and there are even comparisons made to China’s market some years ago. But how much of reality does all this news represent? Are we really growing so fast that a firm valued at $1bn in November 2013, reaches a valuation of $3bn four months later just to reach the $7bn figure only four months after that? The problem is not with the growth of e-commerce. We acknowledge that it is here to stay. But all this rush of money into the system, in a short span of time is what worries us. New investors like Temasek Holdings Pte. Ltd, BlackRock Inc., Government of Singapore Investment Corp., Steadview Capital Management LLc, etc. have pushed up the valuations of a lot of firms in this industry significantly. Are these valuations really justified?

Imagination

Just imagine this. The price of a firm appreciates by more than 600% in less than a year when the industry is itself appreciating at close to 30%. Are all these streams of money leading to a rise in valuations justified by an equivalent growth in the fundamentals? Is the market large enough to actually accommodate so many buyers? When the financial fundamentals in the firms aren’t improving, can we say that this wave is fuelled mainly by investor demand and speculation?

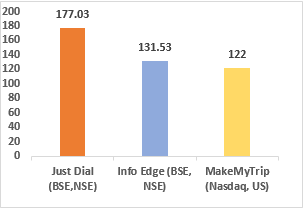

Let us have a look at some e-commerce firms and their valuations:

Flipkart- $ 7 billion

Just Dial- $ 2.08 billion

Info Edge- $ 1.33 billion

Make my Trip- $1.26 billion

The P/E multiples of companies such as Info Edge and Just Dial are on the expensive side at 38 and 55 respectively.

One year increase in stock price (%)

In early 2013, news looked something like this: (Source: LiveMint)

Come 2014, and the story changes dramatically:

Flipkart went from $3 billion in May to $7 billion in July. Snapdeal doubled its value in May after receiving funding. Relatively unknown firms like Fashionandyou and Pepperfry that failed to raise funds last year have garnered funds more than $10 million this year. Why all this hype suddenly? Does it sound too much? Let’s look at how E-commerce firms are valued.

Valuations

The commonly used valuation method is the annualized Gross merchandise value (GMV). As most of the E-commerce firms haven’t made any profits and do not have a positive cash flow, this is used as an approximate estimate for valuation. The GMV is multiplied by about 2-2.5 times to get the valuation of the firm. Flipkart's valuation stands close to 5-7 times the valuation of the firm, which (although not unheard of) is still relatively high for an industry which hasn't yet proved it's credentials.

Indian e-commerce industry is set to grow to $45 billion in the next five years (Nomura Securities). According to IAMAI reports, 70% market share in e-commerce is held by online travel, a majority of which is controlled by IRCTC. The current market share (2013) of Flipkart in Indian E-commerce industry is 5% (Euromonitor International). Assuming that it will sustain this share (despite Amazon), the sales of Flipkart will reach $2.25 billion in 2019. Using the GMV valuation with a multiple of 2.5, the valuation will come up to $5.62 billion. As we can see, the current valuation is 124% of the value it will reach by 2019!

This implies that the growth estimates of the online retail industry do not support the current valuation of Flipkart. The company has anywhere between 15-20 million users as of this year and for the valuation to hold, the number of users should go up to 100 million. When the total number of E-commerce users are estimated to be 100 million by 2020 (Nomura), this expectation seems irrational. Also the business model cannot be ramped up to meet such demand in such a short span. With the infrastructural issues that our country faces, it is not just optimistic, but unrealistic to expect billions of sales in the near future. Investors are not factoring in these constraints. How can we then say that their expectations are in line with reality?

The Indian e-commerce industry is growing at 30% compared to the global average of 8-10%. Investors are willing to pay a premium for the high growth rates in India but are the current valuations sustainable? Investors will not keep pumping cash into firms that don’t earn profits. When Private Equity (PE) and Venture Capital (VC) firms look for short-term investments of 5-10 years, they need a profitable exit route. This quest for profits will make the e-commerce industry undergo further consolidation and only the stronger players will prevail.

Comparisons

Yes, we love to compare ourselves with China every now and then. There are reports suggesting that we are currently where the Chinese market stood in 2007.

Online retail sales in China totalled $296.57 billion in 2013. India had sales of $1.6 billion in 2013 (KPMG). A report by Assocham puts the total retail internet users in China in 2014 at 302 million while that in India at 53.4 million. So, while the number of internet users in China are just around six times that of India, the sales are around 200 times. This is because India has a high amount of ROPOs (Read Online Purchase Offline). This number is estimated at more than 60% according to Assocham reports. There will be arguments stating that these numbers are only set to increase, and that all these people will move online to shop sometime. But what is the incentive for these people to move online? Is it the price advantage or the service advantage? If it is the price advantage, how long can this last? After all, isn’t a business all about making money? Many players in the e-commerce industry are making losses currently. When these e-tailers will be forced to raise prices or reduce the huge discounts currently offered, how sure are we that the same users will purchase online? Is service such an important factor for the Indian consumer that she will be willing to pay a premium for it? Well, for starters, Flipkart recently removed its delivery charges for books, which it had started to charge some time back (For orders less than INR 500). What forced this change? Is there some other factor that all these valuations aren’t factoring in?

Competition

Amazon started its India operations in 2013 and is already emerging as a big player in the online retail segment. Last year, many were of the belief that the era of deep discounts offered by these firms was finally coming to an end. The consolidation that the industry witnessed in further months just corroborated this fact. But as competition intensifies, and as players with deep pockets like Amazon enter the business, it seems as though price wars have started again. After the $1 billion infusion that Flipkart received, Amazon immediately announced a $2 billion investment into its India activities. Also, with Arun Jaitley mentioning in his recent budget speech about “allowing foreign retailers, who manufacture products in the country, to sell via e-commerce platforms”, talks about this being baby steps for allowing FDI in e-commerce have begun. Pressures are rising and if someone like Alibaba enters this business, it is doubtful as to what extent these sky-high valuations will apply. Flipkart has also been recently accused by the government of violating FEMA rules and the claims, if proved, shall set back the firm by a further INR 1400 Crore as fine. At the same time, rumours about Amazon lobbying with government officials to open up e-commerce to global firms are also rife.

Do these valuations consider all these possibilities? Or is the bright light of growth blinding their vision? We believe that growth in the e-commerce industry is here to stay. We also believe that it is essential for a country that is moving towards rapid transformation. But these inflated valuations might just prove detrimental to these firms and to the industry as a whole in the future.

As they say, when the herds go amok, all logic is mere fodder because everyone has set their eyes to ride ‘the bandwagon’.

This article is an entry for the Inside IIM Great B-School debate | Team IIM Trichy

Topic: Valuations in the Indian E-commerce Industry have become irrational

We are arguing for the motion

[caption id="attachment_45243" align="aligncenter" width="300"] Source: Markhamilton consulting[/caption]

Source: Markhamilton consulting[/caption]

Bhanu Putumbaka

Venkat Iyer

The opening arguments AGAINST the motion can be read here - Battle # 1 Valuations in the Indian E-Commerce Industry Have Become Irrational - IIM Ranchi - AGAINST

--------------------

Counterpunch 24 hours later by IIM Ranchi :

Consider the case of Flipkart. The GMV of Flipkart in March 2013 was $ 83 Mn. Taking a multiple of 2.5, the valuation arrives at the figure of $207.5 Mn. Let us see where the current valuation stands: $7 Bn. This can only be arrived at by using a multiple of 84.33!

Though the above quoted analysis by IIM Trichy seems sound and pragmatic with all the numbers and calculations, the projected valuation is NOT that inflated. The GMV is actually calculated in the following way for e-Commerce retail companies:

‘GMV or gross merchandise value for e-commerce retail companies means sale price charged to the customer multiplied by the number of items sold. For example, if a company sells 10 books at Rs 100, the GMV is Rs 1,000. This is also considered as "gross revenue"’. (Economic Times)

In March this year, Flipkart reported annual revenue of $1 Billion. This revenue was backed by sales amounting to 500 Crores INR, which roughly translates to $83 Million. From the gross revenue, it is a short step to deploying a "revenue multiple" between 5 and 7 to arrive at the price Flipkart is valued at in today’s market. Though the multiplier might seem high (the usual norm is 2.5), it is not unheard of.

So, the multiplier used to arrive at the ‘valuation’ is not as inflated as the team from IIM Trichy would have you believe. It is in truth a value that is very much in practice in India. (Business Standard)

When the total number of E-commerce users are estimated to be 100 million by 2020 (Nomura), this expectation seems irrational. Also the business model cannot be ramped up to meet such demand in such a short span. With the infrastructural issues that our country faces, it is not just optimistic, but unrealistic to expect billions of sales in the near future.

The claim made by our opponents that, the estimate of the number of e-Commerce users is ‘irrational’ is not justified. According to Communication and IT Minister Ravi Shankar Prasad’s 1 Lakh Crore INR ‘Digital India’ programme seeks to completely transform the nation into a digitally empowered-knowledge economy. This programme includes among other things a plan to provide high speed internet at Gram Panchayat levels. Additionally this programme envisages a mission to establish broadband highways throughout the country with ‘everywhere mobile connectivity’. All these point to a better infrastructure and a increasing number of internet users in the near future, which in turn will lead to increased e-Commerce activity.

Investors will not keep pumping cash into firms that don’t earn profits. When Private Equity (PE) and Venture Capital (VC) firms look for short-term investments of 5-10 years, they need a profitable exit route. This quest for profits will make the e-commerce industry undergo further consolidation and only the stronger players will prevail.

The above point is quite impertinent to the topic. It is market sales and valuation that are the topics of discussion and not the number of players driving the figures. In fact it is better for the industry as a whole if the investors make sensible decisions and pump money into potential profit guzzlers. This will further ensure that the loss making ventures are weeded out and the rest continue growing. Consolidations are thus welcome rather than being a point of debate.

Also, with Arun Jaitley mentioning in his recent budget speech about “allowing foreign retailers, who manufacture products in the country, to sell via e-commerce platforms”, talks about this being baby steps for allowing FDI in e-commerce have begun. Pressures are rising and if someone like Alibaba enters this business, it is doubtful as to what extent these sky-high valuations will apply.

The opponents basically contend that competition from global players will endanger the survival of Indian players. However, it should be noted that we are talking about the Indian E-commerce industry and this includes or might include any potential foreign subsidiaries as well. For example Amazon, an US based company is operating in India and being counted as a part of the Indian industry. The same will apply if and when Alibaba enters the market. The competition thus generated will only aid to the growth of this industry, justifying the supposed ‘sky-high' valuations.

Moreover, FDI inflow is only a welcome sign as it will lead to huge investments to the tune of billions in ‘Indian e-Commerce industry’. The benefits of FDI have already been covered by us in the original article under Exhibit 1.

When these e-tailers will be forced to raise prices or reduce the huge discounts currently offered, how sure are we that the same users will purchase online? Is service such an important factor for the Indian consumer that she will be willing to pay a premium for it? Well, for starters, Flipkart recently removed its delivery charges for books, which it had started to charge some time back (For orders less than INR 500). What forced this change? Is there some other factor that all these valuations aren’t factoring in?

This is a flawed argument as it only asks open-ended questions without providing any concrete answers about the future consumer behaviour. We can’t possibly predict that consumers don’t or won’t be valuing services very highly. The same argument can be used for our point saying that consumers are indeed moving towards more service intensive companies as prices are becoming increasingly similar. This fact can indeed be corroborated by the huge spurt in sales for Flipkart in the past 3-4 years.

Flipkart removed the delivery charges for the most obvious reason - to counter the growing competition. This is definitely not a cover for something supposedly very shady. With improving infrastructure and better logistics Flipkart might be able to do away with delivery charges without aggravating its current losses.

Team Name: The Intellect Box (IIM Ranchi)

Team Members: Sayan Kar, Adarsh K A M.